In The Aftermath of Disaster

Beginning at about 10:30 AM, on the 30th of December, it is suspected that downed power or communication lines started a grass fire that grew into a firestorm engulfing entire neighborhoods. Some news sources are reporting over 1,000 homes lost. Thankfully, there have been no reports of deaths due to the fire; but, at least two residents remain missing. This conflagration will in the coming days, weeks, months, and (yes, unfortunately) years stress the patience of the residents of Jefferson and Boulder Counties.

The attorneys of the Kanthaka Group were involved in the resolution of many claims that arose from the Waldo Canyon and the Black Forest fires. We hope you will excuse this intrusion, but we would like to offer some suggestions to make the approaching settlement of claims easier.

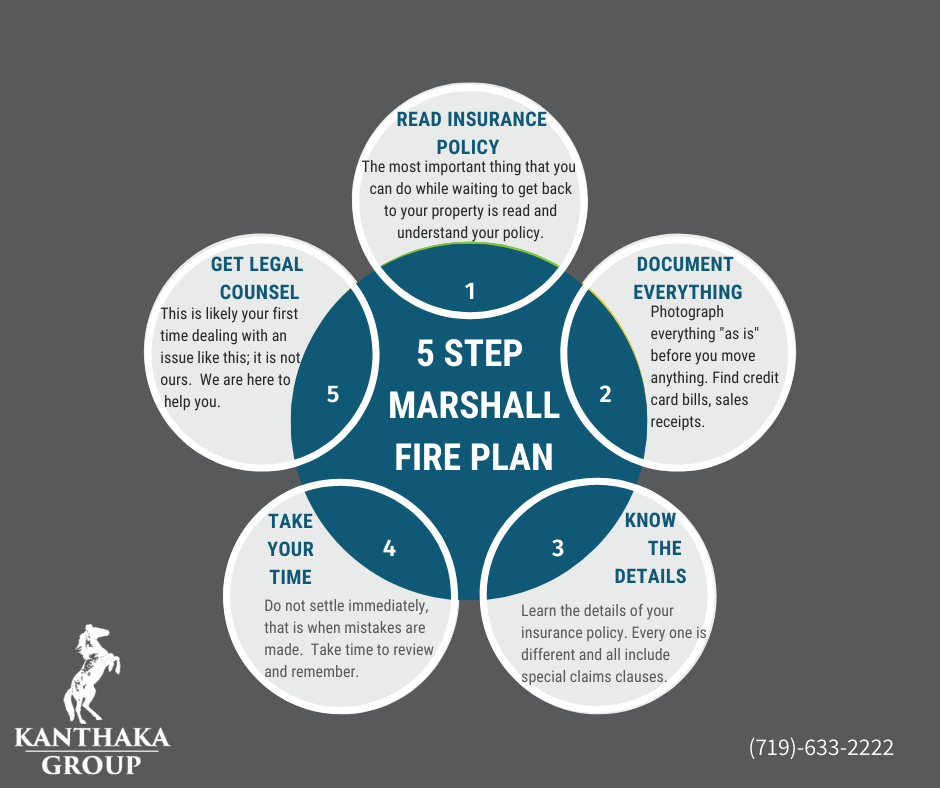

1. READ:

While you and your family are waiting for the “all clear” to return to your home, read your insurance policy and read it again and again. If you don’t understand it, don’t trust the insurance company personnel to explain it to you accurately. Obtain legal counsel for a free consultation. When you make an appointment, the attorney may ask you to send a copy of your insurance policy in advance of a consultation.

2. DOCUMENT, PHOTOGRAPH, and DOCUMENT:

a. Contact your insurance company’s claim department and report that you have suffered a loss. (More about how subtle your loss can be and how losses can expand beyond those areas of flame, in part two.) Obtain written confirmation that you have provided this notice of a claim. Check your policy for how to provide proper notice.

b. Photograph everything before you touch anything. Thirty years ago, with the cost of film and development, there was a constraint on how many pictures folks could afford to take. Not so anymore. Take pictures of everything.

c. And, as you begin this road to recovery, document everything. Get sales receipts for items in your home that you will be making significant claims about – jewelry, firearms, etc. You will at some time be asked for a list of all personal property you lost. One thing we learned, personally with a different fire loss, was that you will continue to remember things to add to the list days after you first go through it. Take your time and always when submitting such a list indicate that it is not a final claim or listing – until you are sure it is.

d. Maintain copious records of every expense you have from 10:30 AM on that awful Thursday until the evening you settle into your new home. Keep and record the receipts for every McDonald’s meal; every night in a hotel; everything you had to buy to get along – toothbrush, a change of clothes, medications.

3. KNOW YOUR POLICY AND CLAIMS:

Earlier we told you that now was the time to read and read again your insurance policy.

a. There are many special types of claims contained in your insurance policies. For example, most policies will have coverage for “additional living expenses” and you should seek an advance on that coverage’s payout. The check for those expenses covered by your insurer should be made out solely to you and not jointly with your mortgage company.

b. Every insurance company’s policy is different; and, there are different ways insurance claims are calculated. Is your policy a “replacement cost” policy or an “actual cash value” policy? While most policies come as replacement cost for the structure; the same is not true of personal property. The difference is the impact of depreciation. Take your 3-year-old dining room table that was purchased for $1000 and today the same or similar table would cost $1500. A replacement cost policy pays $1500; an actual cash value policy might pay only $400, claiming 20% per year depreciation on the purchase price.

4. DON’T SETTLE CLAIMS TOO EARLY:

Insurance companies are not in the business of paying out claims with a smile – despite the commercials. They are in the insurance business to make a profit and to return that profit to shareholders and officers.

a. As indicated before, take your time with personal property claims. The first time you list your personal property losses you will think it was complete…until two days later when you remember the second pair of Maui Jim sunglasses in the dresser. (Personally, when I had a fire loss, I saw my initial personal property list nearly double over the course of the following weeks.)

b. Do not feel rushed into any settlement with your insurance company. Take time to review it and ensure that your claims are complete. For example, some policies include landscaping – did you include the number of blue spruce and strawberry plants in the garden?

c. It is worth the cost to have an attorney review any claims you make or settlements you are offered. Remember that insurance adjusters are in the business of paying claims for the least amount they can – THEY ARE NOT YOUR FRIEND – they are your opponent in a debate overvaluation. The insurance adjusters and claims personnel are well schooled and experienced in handling these claims favorably for the insurance company; they are not your advocate. Insurance companies send out disaster claim teams to “aid in the rapid administration of claims”. Cynically, they want you to settle before you know your losses. You need an advocate.

5. GET LEGAL COUNSEL:

When it comes to compiling, assessing, and settling your claim, it really is a time to seek competent legal counsel. If all is going well with the insurance company, it may only cost you a few hours of the attorney’s time to review and settle the claim. On the other hand, if the insurance company is denying claims or trying to settle for considerably less than what you claim is worth, a lawyer may get more actively involved. Attorneys have a variety of ways to structure fees, in some cases, fees to the attorney could be contingent on the outcome. It’s best to get counsel involved early in the process.

Again, the attorneys at the Kanthaka Group have significant experience and success in representing our clients in settling insurance claims. We are unique in that we understand fire and fire claims. John Scorsine is a long-term volunteer firefighter with experience in major forest fires, including the Black Forest fire. John, and several of Kanthaka Group’s attorneys, have taken that knowledge of fire behavior and coupled it with more general insurance claim work. Let us bring our experience in other disasters to your aid. We offer free consultations and will come to you.